Central banks are about to start rolling back the stimulus they pumped into their economies by buying bonds. For the Bank of England in particular, balance sheet contraction while raising interest rates is taking monetary policy into uncharted territory. Politicians can quickly find themselves in the crosshairs, blamed for worsening the economic downturn they predicted.

The UK central bank, which has already begun a cycle of raising interest rates, is set to accelerate the reduction of its £863 billion ($1.04 trillion) quantitative easing portfolio. In March, it stopped reinvesting maturing debt; it plans to start selling bonds on the secondary market after the September 15 meeting. The problem is that over the past 13 years there has been nothing but more and more quantitative easing, first in response to the global financial crisis and then to sustain growth during the pandemic, no one knows the economic impact of £80bn of annual central bank liquidity withdrawals. The pound - about 100 billion dollars.

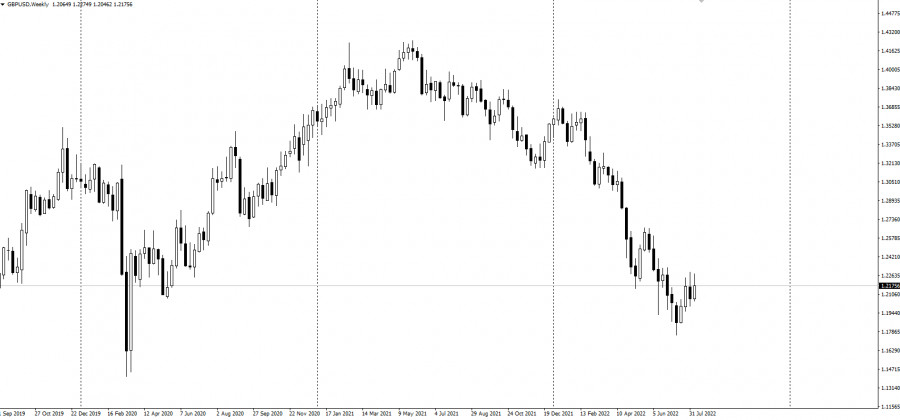

The GBPUSD currency pair has lost 20% since the beginning of the year:

The BoE is very careful to distinguish between its main instrument of interest rate policy and this additional measure of so-called quantitative tightening. While it says it doesn't expect QT to have a big impact on monetary conditions, it's actually speculation. If liquidity in the banking system dries up, it could very easily turn into political football.

This is a dangerous situation: the first two attempts by the Federal Reserve to introduce QT had to be halted and eventually reversed. How smoothly the BoE can cut its balance sheet without triggering a bond market hysteria, with the Fed also trying to write off $95 billion a month from its $9 trillion balance sheet, remains to be seen. One thing is for sure: getting central banks to calculate the effect of rolling their bonds, equivalent to a change in official interest rates, has proved elusive.

The most specific calculation of quantitative easing was made by the former head of the BoE, Mark Carney. In a speech in January 2020, he said that the central bank estimated that every £25bn bond purchases had the same impact as a 25 basis point rate cut. Fed Chairman Jerome Powell calculated at his May 4 press conference that $1 trillion QT is equivalent to one 25 basis point rate hike. This discrepancy speaks eloquently of the slipperiness of the forecast.

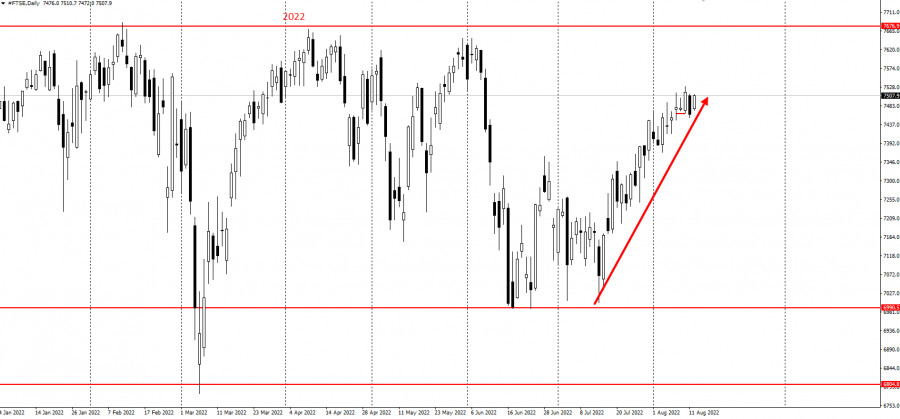

Against this background, the main British stock index continues its rally to the tops of the current year:

The BoE will also get rid of its £19bn of corporate bonds by April 2024. This may seem small compared to the central bank's huge gold holdings, but it could cause secondary turmoil in the pound investment-grade loan market, as it accounts for two-thirds of annual new corporate issuance. This could certainly widen credit spreads and discourage potential issuers if they compete with the central bank for investor demand.

BoE Governor Andrew Bailey signaled that the central bank intends to maintain a sizable bond portfolio, likely as large as the £450bn it held prior to the pandemic emergency support. By 2026, payouts will reduce QE by around £240bn, with strong sales of £160bn easily completing the task. A further reduction in the BoE's balance sheet will come as the support provided directly to banks and corporations in response to the pandemic expires, with the bulk of about £192 billion in debt under the Term Financing Scheme over the next three years. Liquidity in the banking system will have to be managed carefully.

The Monetary Policy Committee says planned bond investment cuts could be put on hold during times of market stress, but Deputy Governor Dave Ramsden said this week there was a "high bar" to stop sales even if the BoE reverses interest rates and will start to reduce the cost of borrowing. More than a decade of ever-growing balance sheets suggests this could be wishful thinking.

Things could go well if the market absorbs the additional supply of gold and the financial sector copes with the liquidity crunch. But the continued reliance on monetary generosity over the past few years hardly inspires confidence that the already struggling UK economy will be able to cope with two obstacles: the removal of stimulus and higher borrowing costs.

Trading analysis offered by RobotFX and Flex EA.

Source

Please do not spam; comments and reviews are verified prior to publishing.